Philip Morris (PM) Q3 Earnings & Revenues Beat Mark, Rise Y/Y

Philip Morris International Inc. PM reported third-quarter 2021 results wherein both the top and the bottom line improved year over year and beat the respective Zacks Consensus Estimate. However, global semiconductor shortage is hampering the supply of IQOS devices.

Philip Morris International Inc. Price, Consensus and EPS Surprise

Philip Morris International Inc. price-consensus-eps-surprise-chart | Philip Morris International Inc. Quote

Quarter in Detail

Adjusted earnings per share came in at $1.58, which beat the Zacks Consensus Estimate of $1.54. Further, the bottom line rallied 11.3% year over year. Excluding currency, the bottom line increased 8.5%.

Net revenues of $8,122 million increased 9.1% from the figure reported in the year-ago quarter. The top line surpassed the Zacks Consensus Estimate of $7,879 million. Net revenues excluding currency improved 7.6%. This upside can be attributed to favorable pricing variance as well as a positive volume/mix. The upsides were partly offset by soft cigarette volumes.

During the quarter, revenues from combustible products were up 1.4% to $5,796 million. Revenues in RRPs increased 34.5% to $2,326 million.

Total cigarette and heated tobacco unit shipment volumes inched up 2.1% to 188.3 billion units. Cigarette shipment volumes slipped 0.4% to 164.8 billion units in the quarter while heated tobacco unit shipment volumes of 23.5 billion units rose 23.8% year over year.

Adjusted operating income came in at $3,549 million, up 9.4% year over year. The metric rose 7.4% on an organic basis. Although adjusted operating income margin of 43.7% rose 0.1 percentage points, the same fell at an equal rate on an organic basis.

Image Source: Zacks Investment Research

Region-Wise Performance

Net revenues in the European Union increased 8.2% to $3,192 million. Net revenues climbed 3.8% on an organic basis, courtesy of improved volume/mix, partly negated by little adverse pricing. Total shipment volumes fell 2.7% to 49,023 million units.

In Eastern Europe, net revenues inched up 4.7% to $941 million. Revenues increased 6.1% on an organic basis, courtesy of a favorable volume/mix and pricing variance. Total shipment volumes rose 2% to 31,139 million units.

In the Middle East & Africa region, net revenues jumped 23% to $945 million. The metric rose 26.6% on an organic basis owing to a positive volume/mix and pricing. Total shipment volumes in the region rose 15% to 35,743 million units.

Revenues in South & Southeast Asia dipped 0.6% to $1,065 million. Revenues in the region slid 1.1% on an organic basis. This downside was a result of adverse volume/mix, partly compensated by a favorable pricing variance. Shipment volumes contracted 4.3% to 35,657 million units.

Revenues from East Asia & Australia advanced 12.2% to $1,523 million. Revenues in the region grew 12.7% organically on a positive volume/mix and pricing variance. Total shipment volumes rose 6% to 20,555 million units.

Revenues from the Americas increased 14% to $456 million. The metric was up 9% on an organic basis on a positive volume/mix and pricing. Moreover, total shipment volumes rose 2.5% to 16,215 million units.

Other Financials

The company ended the quarter with cash and cash equivalents of $4,491 million. It had a long-term debt of $25,768 million and shareholders’ deficit of $8,632 million.

During the quarter, management raised its quarterly dividend by 4.2%, taking the annualized rate to $5 per share. It also bought back 0.9 million shares for $94 million.

Update on IQOS

Management stated that the global semiconductor tightness is causing shortage in supply of IQOS devices, which in turn, is hampering the assortment and availability of these devices in several markets. This was also the reason behind reduced IQOS user growth rates in the third quarter of 2021.

The currently Zacks Rank #4 (Sell) company expects the restrained supply scenario to persist in the first half of 2022. Management laid an emphasis on prioritizing device replacements for the current IQOS users over new device sales. The company expects the user growth rate to pick up again once the semiconductor scarcity situation eases.

Management reiterated its organic compound annual increase goals for net revenues as well as adjusted earnings per share (EPS) of more than 5% and 9%, respectively. Full-year organic growth rate for 2022 is, however, expected to be lower than the 2021-2023 forecast period’s growth expectation due to the IQOS device supply situation.

Guidance

Management now expects full-year earnings per share in the range of $5.77-$5.82 compared with the earlier range of $5.76-$5.86. Adjusted earnings per share for 2021 are now envisioned in the $6.01-$6.06 band.

In 2021, management expects a gradual improvement in the general operating landscape. The company expects a slight recovery in the duty-free business in the fourth quarter with Asia and intercontinental travel being still low. Total cigarette and heated tobacco unit shipment volume growth in 2021 is likely to be 1-2% compared with the flat to 2% rise expected before. Heated tobacco shipment volumes are envisioned to be roughly 95 billion units now compared with 95-100 billion units projected earlier.

For 2021, Phillip Morris expects adjusted net revenues to increase 6.5-7% on an organic basis compared with 6-7% growth anticipated earlier. Adjusted operating margin on an organic basis is likely to expand 200 basis points in 2021.

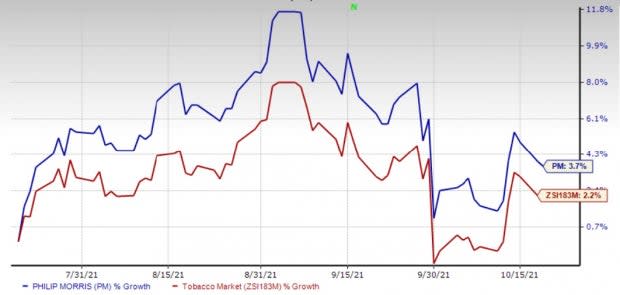

Shares of Phillip Morris have gained 3.7% in the past three months compared with the industry’s rise of 2.2%.

3 Solid Consumer Staple Picks

United Natural Foods, Inc. UNFI currently has a Zacks Rank #1 (Strong Buy) and a trailing four-quarter earnings surprise of 13.1%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

Helen of Troy Limited HELE currently has a Zacks Rank #2 (Buy) and a trailing four-quarter earnings surprise of 19.8%, on average.

The Kraft Heinz Company KHC is currently Zacks #2 Ranked and has a trailing four-quarter earnings surprise of 11.5%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Philip Morris International Inc. (PM) : Free Stock Analysis Report

United Natural Foods, Inc. (UNFI) : Free Stock Analysis Report

Helen of Troy Limited (HELE) : Free Stock Analysis Report

The Kraft Heinz Company (KHC) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research