Walmart Q1 Preview: Can Shares Continue To Display Strength?

Earnings season continues to unwind. It’s been an interesting time so far, with many companies’ quarterly results massively affected by the supply-chain bottlenecks, geopolitical issues, and skyrocketing energy costs that we’ve all become too familiar with.

It’s been one for the ages. We’ve seen some of the top market leaders’ shares plummet following their quarterly releases, which is not typical – stocks generally move upwards during earnings season. It’s safe to say that there has been a massive change in sentiment overall within the market.

Nonetheless, the show rolls on. There are minimal situations, if any at all, when market participants can take a step back for a breather. It’s critical to remain laser-focused, even during times of stress.

A big-time retail giant slated to release its quarterly results before the market opens tomorrow morning is the widely-hailed Walmart WMT.

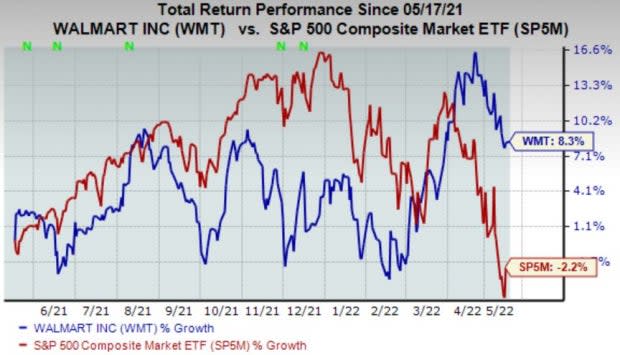

Walmart shares have been a bright spot in an otherwise dim market throughout 2022, providing investors with a respectable 3% return and a much higher blend of valuable defense than the S&P 500, which has declined 15%.

Image Source: Zacks Investment Research

In fact, Walmart shares have displayed great strength throughout the last year as well, providing investors with a return nearly in the double-digits of 8% and easily outpacing the general market.

Image Source: Zacks Investment Research

Investors will be laser-focused on the quarterly results, as Walmart has transformed into one of the biggest retail companies in the world throughout its long history. Let’s dive into how the company is shaping up heading into the report.

Previous Share Reactions & Earnings Results

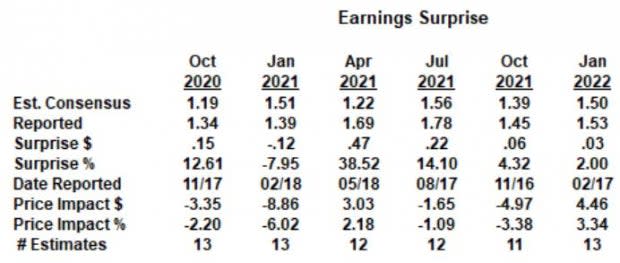

Over its last six quarterly reports, shares have moved upwards just twice following the release of its quarterly results. Both times, shares reacted positively when WMT beat EPS expectations by at least 2%, although shares have also reacted negatively to higher EPS beats. Additionally, shares reacted negatively following the only EPS miss over this timeframe.

Image Source: Zacks Investment Research

The market doesn’t always react very well to EPS beats, and it responds adversely whenever the company reports EPS under expectations. With mixed reactions, it’s challenging to form an accurate data-based prediction of where shares stand to move, but investors should be aware of the overall sentiment leaning negative. Additionally, heading into the report, WMT has an Earnings ESP Score of -2.2%.

Over the last four quarters, the company has beaten earnings expectations each time and has acquired a respectable 15% average EPS surprise. In its latest report, the company exceeded EPS expectations by a slight 2%. Revenue has been on a blazing hot streak, chaining together eight consecutive quarterly revenue beats; in its latest quarter, WMT beat sales estimates by a marginal 1%.

The recent quarterly results do bode well, although the quarter being reported tomorrow comes at a very unique time within our economy as consumers have drastically slowed down their spending.

EPS & Revenue Forecasts

The Zacks Consensus Estimate for the quarter currently sits at $1.46 per share, which displays a decline in earnings of nearly 14% from the year-ago quarter. Over the last 60 days, a singular analyst has revised their quarterly estimate downwards, forcing the Consensus Estimate Trend to retrace by a marginal 0.7%. A year-over-year decline in earnings is a bit concerning, as always. Additionally, higher wages for employees has been a headwind that Walmart has been facing.

Revenue estimates for the quarter appear a bit stagnant. The $138.2 billion Zacks Consensus Sales Estimate reflects a very marginal decline of 0.03% compared to the year-ago quarter whenever Walmart raked in $138.3 billion. WMT is known for raking in an immense amount of cash, but again, a year-over-year decline in revenue raises questions heading into the quarterly report.

Bottom Line

Overall, quarterly estimates heading into the report reflect a slowdown in both the top and bottom line. Additionally, the company has a negative Earnings ESP score heading into the quarterly report and is currently ranked as a Zacks Rank #4 (Sell). I believe that it is beneficial for investors to heed caution heading into the report for these reasons.

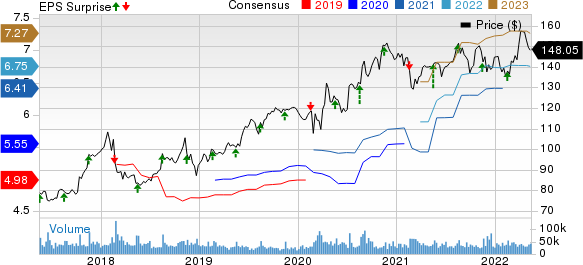

Walmart Inc. Price, Consensus and EPS Surprise

Walmart Inc. price-consensus-eps-surprise-chart | Walmart Inc. Quote

Instead, I think that investors should take a closer look at Costco Wholesale Corporation COST. The company boasts a higher forward earnings multiple than WMT, but there have been positive EPS estimate revisions across the board.

Image Source: Zacks Investment Research

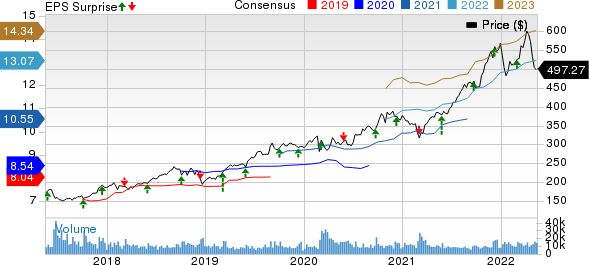

Over the last 60 days, the Consensus Estimate Trend for the upcoming quarter has increased by 2.4%, reflecting earnings growth in the double-digits at 11% from the year-ago quarter. Furthermore, COST’s earnings for the current year are expected to grow by a solid 18% year-over-year.

Revenue for the quarter is expected to climb 15% from the year-ago quarter, and full-year sales estimates for the current year display a 14% expansion in the top line.

COST has acquired a very respectable 14% average EPS surprise over its last four quarters, and in its most recent quarter, the company exceeded EPS estimates by nearly 9%. Furthermore, Costco boasts a Zacks Rank #2 (Buy), which further instills a great deal of confidence in the company’s share performance moving forward.

Costco Wholesale Corporation Price, Consensus and EPS Surprise

Costco Wholesale Corporation price-consensus-eps-surprise-chart | Costco Wholesale Corporation Quote

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Walmart Inc. (WMT) : Free Stock Analysis Report

Costco Wholesale Corporation (COST) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research