Here's Why You Should Retain Abbott (ABT) Stock for Now

Abbott Laboratories ABT is well-poised for growth in the coming quarters, courtesy of its continued growth in the core Diagnostics arm. Solid fourth-quarter 2022 performance buoys optimism. However, forex woes and Nutrition Product recall are impeding growth.

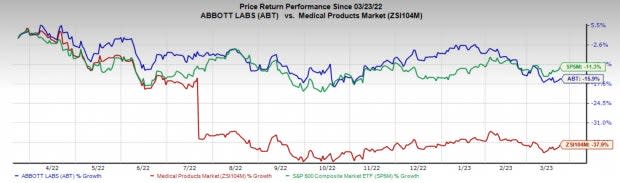

In the past year, this Zacks Rank #3 (Hold) stock has lost 15.9% compared with a 37.9% decline of the industry and a 11.3% fall of the S&P 500 composite.

This renowned provider of a diversified line of healthcare products has a market capitalization of $170.89 billion. The company projects 5.1% growth for the next five years and expects to maintain its strong performance. Abbott’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 22.42%.

Let’s delve deeper.

Q4 Upsides: Abbott exited the fourth quarter of 2022 with better-than-expected earnings and revenues. Excluding COVID testing sales, worldwide Diagnostics sales grew over 11% in the fourth quarter. Growth in the quarter was led by rapid diagnostics where, excluding COVID-19 tests, sales improved 30% year over year. Within EPD, sales increased 8% organically in the fourth quarter, led by double-digit growth. In Medical Device, sales rose 7.5% globally. In the United States, sales growth was led by double-digit growth in Electrophysiology, Structural Heart and Diabetes Care. Within Diabetes Care specifically, fourth-quarter sales of FreeStyle Libre grew over 40% in the United States and global Libre sales reached $4.3 billion for 2022.

Core Diagnostics Grow Strong: In Diagnostics, COVID testing sales were $1.1 billion in the fourth quarter. Excluding COVID testing sales, worldwide diagnostics grew over 11% in the quarter. Growth in the quarter was led by rapid diagnostics where, excluding COVID-19 tests, sales improved 30% year over year. During the pandemic, Abbott significantly expanded the install base of ID NOW and opened new testing channels. This expanded footprint drove strong growth and supported testing needs when flu and other respiratory infections surged late in 2021. During 2022, Abbott continued with the rollout of Alinity, the company’s innovative suite of diagnostic instruments, and expand test menus across its platforms for immunoassay, clinical chemistry and molecular testing.

Image Source: Zacks Investment Research

Progress With Diabetes Business: This business achieved organic sales growth of 17.3% in the fourth quarter of 2022 led by strong growth in FreeStyle Libre. In the quarter, sales of FreeStyle Libre were $1.1 billion. In the United States, where sales grew more than 40%, the company initiated the full launch of Libre 3. This latest device can automatically deliver up-to-the-minute glucose readings with more accuracy in the world’s smallest and thinnest wearable sensor. Abbott’s Libre sales reached $4.3 billion for the full-year 2022.

Downsides

Foreign Exchange Translation Impacts Sales: Foreign exchange is a major headwind for Abbott due to a considerable percentage of its revenues from outside the United States. The strengthening of the Euro and some other developed market currencies have constantly been hampering the company’s performance in the international markets.

Nutrition Product Recall Impedes Growth: Within Abbott’s Nutrition business, in the fourth quarter, worldwide Nutrition sales were down 5.7% on an organic basis, with an 11.8% slump in Pediatric Nutrition sales. The downside in worldwide Nutrition and Pediatric Nutrition sales can be attributed to a voluntary recall and manufacturing shutdown of certain infant formula products manufactured at one of Abbott's U.S. plants since last February.

Estimate Trend

Abbott has been witnessing a negative estimate revision trend for 2023. In the past 90 days, the Zacks Consensus Estimate for its earnings has moved 0.5% down to $4.38.

The Zacks Consensus Estimate for the company’s 2023 revenues is pegged at $39.74 billion, suggesting an 8.9% decline from the year-ago quarter’s reported number.

Key Picks

Some better-ranked stocks in the broader medical space are Hologic, Inc. HOLX, Henry Schein, Inc. HSIC and Avanos Medical, Inc. AVNS.

Hologic, carrying a Zacks Rank #2 (Buy) at present, has an estimated long-term growth rate of 15.2%. HOLX’s earnings surpassed the Zacks Consensus Estimate in all the trailing four quarters, the average beat being 30.6%.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Hologic has gained 1.7% against the industry’s 17.5% growth in the past year.

Henry Schein, carrying a Zacks Rank #2 at present, has an estimated long-term growth rate of 8.1%. HSIC’s earnings surpassed estimates in three of the trailing four quarters and matched the same in the other, the average beat being 2.9%.

Henry Schein has lost 12.4% compared with the industry’s 10.9% decline over the past year.

Avanos, carrying a Zacks Rank #2 at present, has an estimated growth rate of 1.8% for 2023. AVNS’ earnings surpassed estimates in all the trailing four quarters, the average beat being 11%.

Avanos has lost 13.7% compared with the industry’s 17.5% decline over the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Abbott Laboratories (ABT) : Free Stock Analysis Report

Hologic, Inc. (HOLX) : Free Stock Analysis Report

Henry Schein, Inc. (HSIC) : Free Stock Analysis Report

AVANOS MEDICAL, INC. (AVNS) : Free Stock Analysis Report