I mostly cover dividend-paying stocks, and while I believe they should be the cornerstone of most investment portfolios, quality growth names shouldn't be ignored. That's because growth stocks are admittedly more tax-efficient, since reinvested capital isn't taxed in the same manner that dividends are at the individual level.

In this article, I'm focused on Hologic (NASDAQ:HOLX), which has seen impressive growth over the past year. I highlight why Hologic is a worthy Buy at present, despite some challenges that may arise next year, so let's get started.

Why HOLX Is A Buy

Hologic is a medical technology company that's primarily focused on women's health through early detection and screening. This includes breast health solutions that includes screening, biopsies, surgical imaging, and treatment/monitoring. It also includes diagnostics, gynecological surgical products, and skeletal solutions to measure bone density. In the trailing 12 months, HOLX generated $4.2 billion in total revenue.

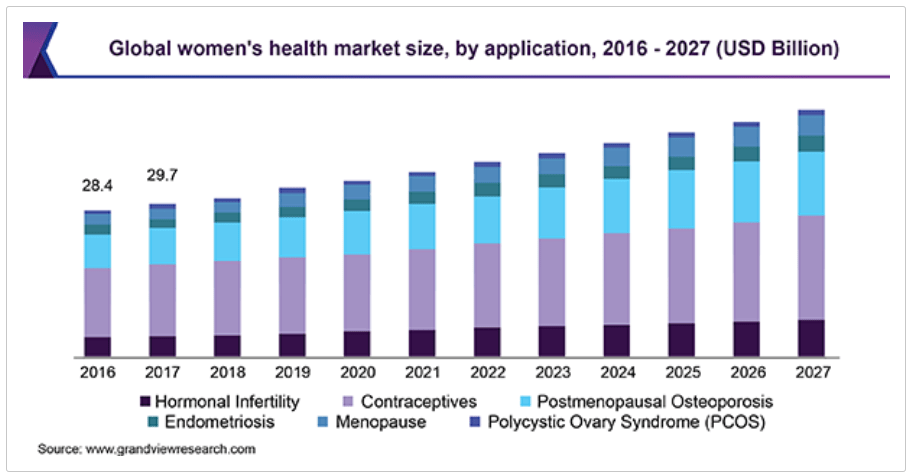

Healthcare is an attractive investment sector to be in, and the women's health segment is no different. This is supported by research showing that the global women's health market size was around $33 billion in 2020.

It remains an underserved market, however, and is expected to grow at a robust 4.9% CAGR between now and 2027, driven by the categories as seen below. HOLX should be able to participate in this growth with its diagnostics and surgical solutions that pertain to some of these areas.

(Source: Grandview Research)

Meanwhile, HOLX has demonstrated robust growth in its latest Q3'21 results (ended June 2021), with revenue growing by 38% YoY on a constant currency basis. This was driven by a growth in the company's Breast and Skeletal Health and GYN Surgical divisions compared to the prior-year period, when many doctor office visits were postponed due to COVID-19. This growth more than offset the decline in 2 COVID assays that run on HOLX's Panther and Panther Fusion systems.

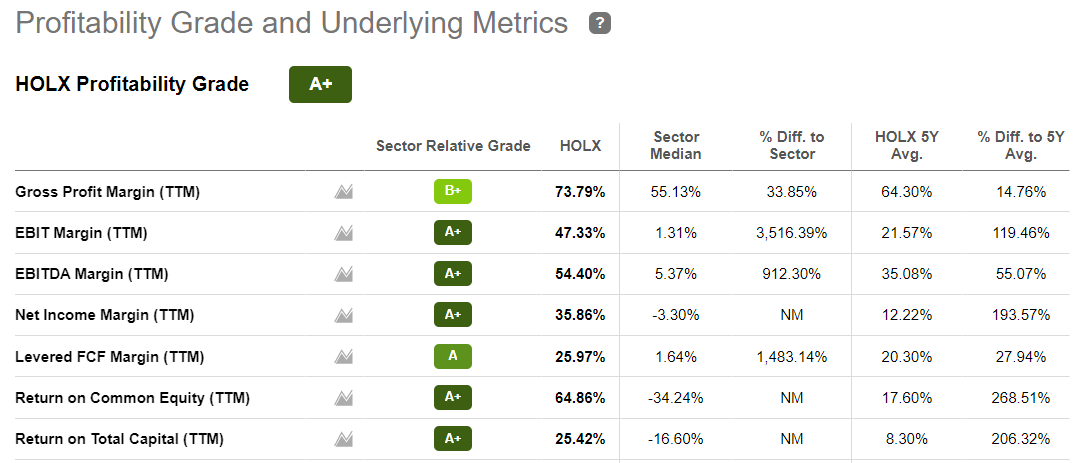

I'm also encouraged to see Q3'21 gross margin increasing by 140 bps YoY, to 66.1%, as HOLX saw a volume recovery in its base business, while still seeing meaningful contribution from sales of its COVID test. This, combined with cuts in operating spend, resulted in operating margin improving by an impressive 650 bps YoY, to 39.5%. As seen below, HOLX maintains class-leading margins, earning it an A+ grade for Profitability from Seeking Alpha.

(Source: Seeking Alpha)

Looking forward, I see HOLX emerging from the pandemic as a stronger and faster-growing company. This is considering the cash windfall that it received from proving COVID test over the past 15 months, resulting in operating cash flow of $2.5 billion over the trailing 5 quarters and $2.3 billion over TTM, comparing favorably to the $650 million operating cash flow that it achieved in FY 2019 (pre-COVID)

I see management making good use of this cash, as it used $1.35 billion to buy six companies, including $808M for Finnish molecular diagnostics company, Mobidiag, and spent $510 million on share buybacks. These acquisitions further diversify HOLX's product offerings and enable it to capture growth areas. This is supported by management's comments on recent acquisitions and the internal R&D pipeline during the earnings conference call:

First, Biotheranostics enables us to enter the lab-based oncology space, a long time area of interest that has been growing rapidly. Biotheranostics is off to an excellent start with about $13 million of revenue in the third quarter, more than 30% higher than their best quarter prior to the pandemic.

Second, Diagenode will help us add PCR-based menu to our Panther Fusion instrument, both in Europe and the United States. And third, the acquisition of Mobidiag enables us to enter the rapidly growing market for acute care, near-patient testing, which we have been monitoring for years.

Another reason we feel confident in Surgical's future is the revitalization of our R&D pipeline. A few years ago, the division was basically a two-product show. Today, however, we sell multiple versions of these products, as well as new fluid management system, hysteroscopes and other GYN surgical tools and we have a robust pipeline of new products in development.

Balance Sheet and Valuation

HOLX maintains a strong balance sheet, with $828 million in cash on hand, and a net debt to EBITDA of 0.75x. While the leverage ratio is low due to benefits from COVID tests, I would expect for it to be at the 2.0x level or lower in a post-pandemic world, as EBITDA contributions from the recent acquisitions ramp up.

Turning to valuation, HOLX appears to be cheap at the current price of $74.25 with a forward PE of 9.6. This is due in part to earnings benefits that HOLX received from COVID tests, and analysts expect earnings to be $4.00 next year, equating to a forward PE of 18 based on 2022 earnings.

I believe this may be a bit too conservative, however, considering the recent acquisitions and internal R&D pipeline mentioned earlier, which should contribute to earnings. As such, I wouldn't be surprised to see upward revisions by analysts following the recent earnings release.

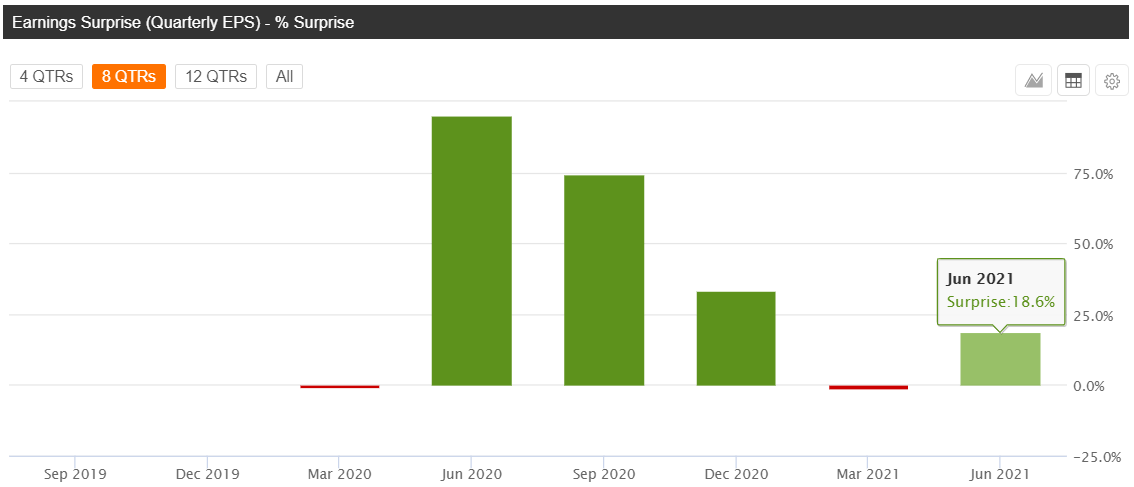

Plus, as seen below, HOLX has given earnings surprises in 4 of the past 8 quarters, with all 4 beating estimates by a material percentage. Lastly, despite lower earnings expectations for next year, analysts still have a Buy rating on HOLX with an $81.50 price target.

(Source: Seeking Alpha)

Of course, no investment is risk-free, and the following points should be considered:

- HOLX's recent acquisitions come with integration risk, and there's always the chance that they don't live up to expectations.

- A faster-than-expected ramp-down in COVID tests would impact near-term profitability. However, that doesn't change the long-term thesis.

- Competitive pressures could reduce margins and impact the bottom line.

Investor Takeaway

Hologic has carved out a strong name for itself in Women's Health, and is set to benefit from the long-term growth trend of this segment. It's seeing a strong rebound in its core business, and management is making the most of its 'COVID windfall' by making strategic investments.

As such, I see Hologic emerging from the pandemic as a stronger enterprise. Meanwhile, HOLX maintains a strong balance sheet, and I believe the market is underestimating its growth potential. HOLX is a Buy for growth.