The Price Is Right For SUSE S.A. (ETR:SUSE) Even After Diving 30%

SUSE S.A. (ETR:SUSE) shares have retraced a considerable 30% in the last month, reversing a fair amount of their solid recent performance. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 36% share price drop.

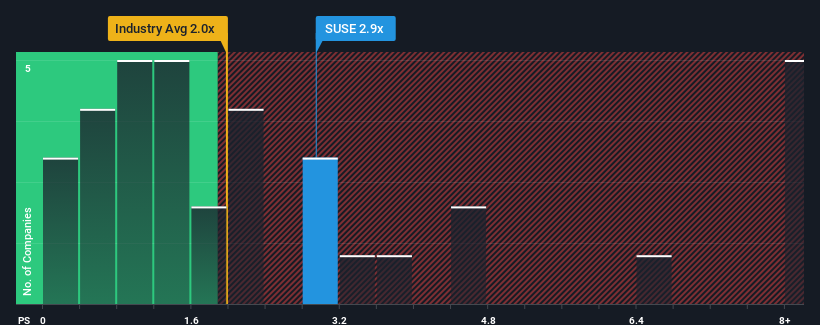

In spite of the heavy fall in price, you could still be forgiven for thinking SUSE is a stock not worth researching with a price-to-sales ratios (or "P/S") of 2.9x, considering almost half the companies in Germany's Software industry have P/S ratios below 2x. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

Check out our latest analysis for SUSE

What Does SUSE's Recent Performance Look Like?

SUSE could be doing better as it's been growing revenue less than most other companies lately. It might be that many expect the uninspiring revenue performance to recover significantly, which has kept the P/S ratio from collapsing. If not, then existing shareholders may be very nervous about the viability of the share price.

Want the full picture on analyst estimates for the company? Then our free report on SUSE will help you uncover what's on the horizon.

How Is SUSE's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as high as SUSE's is when the company's growth is on track to outshine the industry.

Retrospectively, the last year delivered a decent 5.9% gain to the company's revenues. Pleasingly, revenue has also lifted 50% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing revenues over that time.

Looking ahead now, revenue is anticipated to climb by 6.4% during the coming year according to the six analysts following the company. Meanwhile, the rest of the industry is forecast to only expand by 3.6%, which is noticeably less attractive.

With this information, we can see why SUSE is trading at such a high P/S compared to the industry. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

What We Can Learn From SUSE's P/S?

Despite the recent share price weakness, SUSE's P/S remains higher than most other companies in the industry. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our look into SUSE shows that its P/S ratio remains high on the merit of its strong future revenues. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. It's hard to see the share price falling strongly in the near future under these circumstances.

You should always think about risks. Case in point, we've spotted 2 warning signs for SUSE you should be aware of, and 1 of them shouldn't be ignored.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.