Here's What To Make Of Myer Holdings' (ASX:MYR) Decelerating Rates Of Return

There are a few key trends to look for if we want to identify the next multi-bagger. In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. However, after investigating Myer Holdings (ASX:MYR), we don't think it's current trends fit the mold of a multi-bagger.

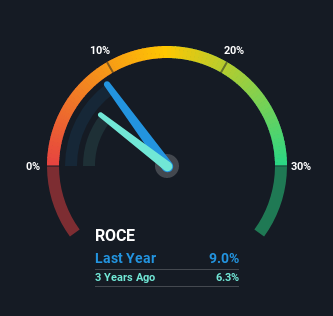

What is Return On Capital Employed (ROCE)?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. To calculate this metric for Myer Holdings, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.09 = AU$168m ÷ (AU$2.5b - AU$590m) (Based on the trailing twelve months to July 2021).

So, Myer Holdings has an ROCE of 9.0%. In absolute terms, that's a low return and it also under-performs the Multiline Retail industry average of 20%.

Check out our latest analysis for Myer Holdings

Above you can see how the current ROCE for Myer Holdings compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Myer Holdings.

The Trend Of ROCE

The returns on capital haven't changed much for Myer Holdings in recent years. The company has consistently earned 9.0% for the last five years, and the capital employed within the business has risen 31% in that time. Given the company has increased the amount of capital employed, it appears the investments that have been made simply don't provide a high return on capital.

The Key Takeaway

In conclusion, Myer Holdings has been investing more capital into the business, but returns on that capital haven't increased. Since the stock has declined 66% over the last five years, investors may not be too optimistic on this trend improving either. All in all, the inherent trends aren't typical of multi-baggers, so if that's what you're after, we think you might have more luck elsewhere.

Myer Holdings does come with some risks though, we found 2 warning signs in our investment analysis, and 1 of those is concerning...

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.